Protein demand is hotter than ever, but not all proteins are created equal. Why more strategic protein innovators will be the ultimate winners in the GLP-1 nutrition space.

The Protein Gold Rush

The protein gold rush has CPG brands adding whey to everything from candy bars to pasta sauce. Convincing healthy people they need 40 grams of protein in their morning coffee can hardly be considered innovation – it’s just clever marketing. Companies are creating solutions for problems that don’t exist while ignoring a real, substantially more promising and profitable opportunity.

This explosion of high-protein everything is driven by influencer marketing and social media trends. Brand companies – essentially marketing entities that own no factories or equipment – ride these trends by contracting out production. When the trend fades, they’ll simply launch new brands to chase the next fad.

Meanwhile, ingredient suppliers invested heavily in protein production capacity to meet this hype-driven demand are now in desperate search of new applications. Most recently, the plant-based boom left these companies with specialized facilities, advanced protein processing capabilities, and long-term supply contracts, but plateauing demand.

The companies that are actually responsible for making real things in the real world – i.e., ingredient suppliers and co-manufacturers – have learned to serve whatever trend brand companies are chasing this quarter. They invest just enough capacity for today’s fad, knowing tomorrow will bring something different. This dynamic constrains genuine innovation. Why develop precise purification systems that maintain functionality when your customers’ marketing departments only care about riding the current hype train?

Current and former GLP-1 users are real people whose quality of life is directly tied to the food they consume. They need nutritionally dense food, not products plastered with meaningless claims. For companies tired of chasing fads, this represents something rare: medical need driving sustained demand. This is the market that justifies real innovation – where functionality and clinical outcomes matter more than marketing claims, where customers will pay premiums for products that actually work.

GLP-1s: A Tale of Two Markets

The rise of GLP-1 medications has created two distinct populations with urgent nutritional needs that standard protein products ignore.

Current Users: The Immediate Challenge

Muscle loss: Up to one-third of weight loss comes from lean tissue, not fat 1

Severe portion limits: Can only manage 4-6 oz of food per meal

GI sensitivity: Cannot tolerate traditional high-fiber foods or standard protein sources

Nutrient density imperative: With drastically reduced intake, every bite must deliver maximum nutrition

Former Users: The Growing Opportunity

85% discontinue within two years due to cost and insurance barriers 2

The protein-fortified food industry has mastered marketing but ignores quality. Most products deliver poor-quality protein that the body can barely use.

Here’s what matters: PDCAAS (Protein Digestibility Corrected Amino Acid Score) measures true protein quality. A score of 1.0 means optimal quality. Most trendy protein products don’t come close because high-quality protein is expensive, and the average consumer buying a protein cookie isn’t checking amino acid profiles.

This works when your customers are healthy people who don’t need extra protein. Most Americans already consume excessive protein. But GLP-1 users face genuine muscle loss risks and need products designed for medical nutrition, not Instagram appeal.

Key failures of current products:

Poor protein quality: PDCAAS scores of 0.1-0.2 when optimal is 1.0

Wrong format: 12-oz shakes when users can only manage 4-6 oz

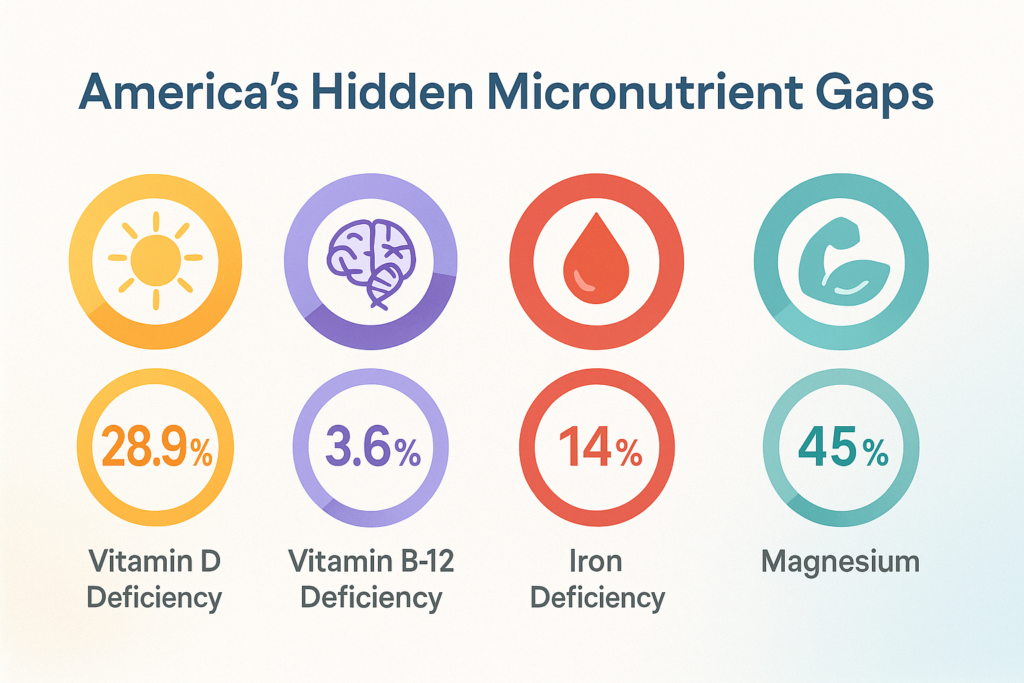

Iron: 14 % of U.S. adults have absolute iron deficiency 7

Magnesium: ~45 % of Americans consume below the estimated average requirement 8

Ignores GI sensitivity: Denatured proteins slow digestion and reduce bioavailability; when fiber is present, it’s typically bulk-forming types that worsen symptoms by binding water, creating gas, thus slowing down already-slowed digestive systems

If an ingredient supplier develops proteins with optimized amino acid profiles and enhanced digestibility, they certainly won’t be advertising PDCAAS scores on TikTok. The non-medical market rewards trendy labels over technical specifications.

The High-Protein Market Opportunity

By The Numbers

By early 2024, roughly one in eight American adults had used a GLP-1 medication 9 – unprecedented adoption for a prescription obesity treatment. With 30 million Americans having tried GLP-1s 10 and an 85% discontinuation rate, we face a projected population of 25 million post-GLP-1 users within the next few years.

These aren’t casual dieters. They’ve experienced pharmaceutical-grade results and understand the stakes. Most importantly, their experience paying $1,200-1,500 monthly for medication creates powerful price anchoring. A specialized functional food program costing $150-200 monthly ought to be affordable by comparison.

Intersecting Opportunities

Regulatory catalyst: The FDA’s recent declaration ending GLP-1 shortages 11 access to affordable compounded versions. Millions must now choose between paying full price or discontinuing treatment.

Supply meets demand: Ingredient suppliers with excess capacity from the plant-based boom 12,13 possess the technical capabilities to create clinical-grade ingredients – they just need a market that values quality over marketing.

No dominant player:

Sports nutrition brands focus on athletes seeking muscle gains (supplements for enhancement, not medical needs)

Weight loss companies push meal replacements and appetite suppressants (often high fiber formulas that worsen GI distress)

Medical nutrition serves hospital patients with specific clinical protocols (requires prescription, too narrow for broad GLP-1 population)

None of these directly address the unique needs of current or former GLP-1 users – yet all the necessary components exist across these markets. This gap creates an opportunity for companies willing to combine clinical-grade quality with consumer-friendly formats.

Why Most Companies Will Miss This

Brand companies chasing protein trends are structurally unsuited for medical nutrition:

R&D priorities: Focus on taste and broad market appeal, not therapeutic efficacy

Distribution models: Built for high-velocity mass market, not premium, specialized products

Marketing metrics: Reward shelf turns and market share, not health outcomes

The short-term trap: Chasing quick profits through trendy products guarantees commodity pricing and thin margins. High-margin opportunities require long-term investment in clinical validation and precise manufacturing – commitments that quarterly-focused companies won’t make

The companies that recognize this gap – and have the technical capability to bridge it – will define the next decade of functional food.

The Path to Prosperity

Success in this market requires rethinking fundamental assumptions about product design:

Format is everything: Products must work within 4-6 oz portion limits while delivering the 25-30g of quality protein needed per meal to stimulate muscle protein synthesis 14. Plus, they need to include essential micronutrients.

Quality over marketing: Pre-digested proteins, gentle fibers, bioavailable micronutrients – the ingredients that matter won’t fit on a trendy label.

Distribution strategy: Direct-to-consumer or specialty channels that allow for education and premium pricing.

Companies positioned to win aren’t necessarily those with medical food experience – they’re those willing to treat this as the medical nutrition challenge it is. A nimble contract manufacturer could partner with the right brand. An innovative ingredient supplier could develop turnkey solutions.

Seize the Moment

The market is developing rapidly. Regulatory changes and discontinuation patterns are creating new cohorts of former users each month.

The convergence of opportunities makes the current moment a unique – and fleeting – one:

25 million consumers with proven premium spending capacity

Ingredient suppliers with excess capacity and technical capabilities

No established market leader

Innovation comes from combining three successful models (D2C distribution, medical nutrition, premium pricing) to create a new product category

For ingredient suppliers and contract manufacturers tired of chasing quarterly fads, this represents something rare: a chance to build lasting value by solving real problems.

The question isn’t whether this market will develop – it’s who will capture it first.

Interested in exploring how your capabilities could serve this emerging market?

Contact David Goulder to discuss the technical and market requirements necessary to seize this moment.

Lance Lively is the Founder of The Gut Punch, a platform investigating the intersection of food and health. He’s served as a senior leader at a number of venture-backed biotechnology companies. A Princeton and Wharton graduate, he focuses on human health, novel modalities to improve wellness, and the science of addiction.

David Goulder is the founder of Food Science and Applied Research Consulting, with 11 years of experience in food science and technology. He works at the intersection of science, strategy, and product development – helping teams solve complex technical challenges efficiently, from ingredient functionality and formulation to integrating new research and scaling innovation. David holds a BS and MS in Food Science and Technology.

My interview with Marc Washington, Founder & Executive Chairman of SuperGut.

SuperGut: Marc Washington

What separates a truly transformative health brand from the endless sea of wellness products promising to cure all maladies?

Why do some founders build category-defining companies, while others with nearly identical ingredients fade into obscurity?

And what happens when years of scientific groundwork suddenly collide with a metabolic revolution that completely reshapes people’s relationships with food?

In case you haven’t noticed, fiber and GLP-1s are both having major cultural moments. And SuperGut, whether through prescience or providence, spent years developing gut-healthy fiber blends and conducting gold-standard clinical trials – long before Ozempic became a household name.

I recently joined Alex Shandrovsky, host of the Investment Climate Podcast, for a conversation with Marc Washington, founder and executive chairman of SuperGut.

Our discussion digs into the balancing act between scientific rigor and market momentum, the hard decisions around investing in clinical validation versus splashy marketing, and what it takes to carve out real differentiation in a world where a new “natural GLP-1” copycat emerges every week.

And as Marc transitions from CEO to Executive Chairman, we tackle the ultimate question that haunts every founder as they hand over the reins: how will you know whether you’ve built an enduring brand that will stand the test of time?

Inside America’s broken drug pricing system, and why health insurers are the men behind the curtain

There’s More to Drug Pricing than Meets the Eye

In last month’s investigation, we exposed the devastating impact of the FDA’s decision to end access to compounded GLP-1 alternatives, forcing millions of Americans to confront the shocking reality of $1,000+ monthly price tags for brand-name weight loss and diabetes medications.

We explained how manufacturers set astronomical list prices, how other countries pay a fraction of what Americans pay, and how insurers rarely cover these drugs for obesity despite their proven effectiveness.

But there’s another critical piece to this affordability puzzle: the hidden middlemen.

The Hidden Layer

While pharmaceutical manufacturers like Novo Nordisk and Eli Lilly certainly bear responsibility for setting high list prices for drugs like Ozempic, Wegovy, Mounjaro, and Zepbound, a complex and opaque network of intermediaries – particularly Pharmacy Benefit Managers (PBMs) – wields extraordinary influence over what patients ultimately pay and whether they can access these medications at all.

Drugmakers argue that U.S. prices are high because of the unique American system of rebates and middlemen. In a 2024 Senate hearing, Novo Nordisk’s CEO testified that “we pay 75 cents of every dollar of medicine we sell back into this complex system in rebates, discounts, and fees.” 1 In other words, only 25% of the gross revenue from Ozempic/Wegovy might actually be kept by Novo Nordisk; the rest is absorbed by intermediaries in the supply chain.

That “complex system” includes PBMs negotiating rebates, insurers and Third-Party Administrators (TPAs) administering plans, and brokers steering employer insurance plan decisions. Each intermediary takes a slice.

When competition is limited (as with brand-name GLP-1s under patent) and cheaper workarounds like compounding are eliminated, the leverage of these middle players grows. With no low-cost alternative available, all transactions must flow through the standard distribution and insurance channels – where middlemen can impose their mark-ups, fees, or negotiated spreads.

The result is a U.S. market where list prices soar, even if net prices after rebates are somewhat lower – and patients without strong insurance coverage can be left with unaffordable bills.

Pharmacy benefit managers (PBMs) are often singled out in discussions of high drug costs – and for good reason. PBMs manage prescription drug benefits for insurers and employers, deciding which drugs are covered (formularies) and negotiating rebates and discounts with drug manufacturers.

Health plans (i.e. employers and insurers) often choose PBM services based on criteria like rebate guarantees, formulary breadth, and administrative cost, which pressures PBMs to maximize rebates. PBMs also compete to secure exclusive arrangements with large buyers by offering bigger savings, which often means bigger rebates.

In theory, PBMs are meant to leverage volume to lower net costs for health plans. In practice, their business model can create perverse incentives that inflate list prices.

Rebate Structures and Formulary Control

PBMs typically negotiate hefty rebates from manufacturers of expensive brand-name drugs in exchange for favorable placement on the formulary, a list of medications that a specific health insurance plan or PBM covers.

These rebates are paid by the manufacturer to the PBM after the sale and are often a percentage of the drug’s list price. This means a PBM’s revenue from a drug can increase if the manufacturer raises the list price, since a higher price yields a larger rebate (even though the net price to the insurer and insured patients may remain unchanged).

According to an FTC investigation, the “Big Three” PBMs (CVS Caremark, Express Scripts, and OptumRx) – which together manage about 80% of U.S. prescriptions 2 – have created a “perverse drug rebate system” that prioritizes high rebates over low list prices 3.

Case Study: Insulin

The FTC’s 2024 complaint against PBMs alleges they “rigged” the system so that drugs with higher list prices (and thus higher rebates) are favored, while lower-list-price alternatives are excluded, ultimately artificially inflating drug costs 4.

In the case of insulin, even when lower-priced versions came to market, PBMs kept them off formularies in favor of higher-priced, rebated products. This strategy allowed PBMs and their affiliated rebate intermediaries to “line their pockets while patients are forced to pay higher out-of-pocket costs,” according to the FTC 5.

Pricing Power and Rebate Walls

Because PBMs control formulary access for millions of patients, manufacturers feel compelled to offer large rebates to secure or maintain favorable placement. A high-demand drug like a GLP-1 agonist effectively faces a “pay-to-play” system.

If Novo Nordisk or Eli Lilly didn’t offer substantial rebates, a PBM could exclude their drug or put it on a higher copay tier in favor of a competitor that offers a bigger rebate. This has led to what some call “rebate walls,” 6 where dominant products (with high list prices and rebates) block cheaper would-be rivals from getting traction.

The result is inflated list prices across the board. So long as PBMs are evaluated by plan sponsors on how much rebate dollars they secure, they have a motivation to prefer high-price/high-rebate drugs to lower-cost drugs that don’t throw off as much rebate, even if the lower-cost drug might save the health plan money overall.

So… Who Owns the PBMs?

The largest PBMs have merged with insurance companies and pharmacy chains (surprise!), creating massive healthcare conglomerates:

CVS Caremark is part of CVS Health, which owns Aetna insurance and CVS pharmacies

Express Scripts is owned by Cigna

OptumRx is part of UnitedHealth Group

This integration creates additional profit opportunities. PBMs steer patients to higher-revenue drugs while blocking competitor pharmacies from offering discounts 7.

Application to GLP-1 Drugs

For GLP-1 medications, manufacturers have openly asserted that a similar perverse dynamic is at play. Lars Fruergaard Jørgensen, CEO of Novo Nordisk, testified during a U.S. Senate hearing that the high U.S. list price for Ozempic/Wegovy was driven by PBM negotiations, not production costs 8.

Jørgensen noted that simply lowering the list price would likely backfire because PBMs “often limit access to drugs with lower list prices because they receive less financial benefit from them.” 9 This rebate-driven distortion is a key reason U.S. prices are far above those in Europe, where such rebate middlemen play a smaller role.

The PBM industry argues that manufacturers alone set the prices and that PBMs actually return most savings to patients or payers. In the recent Senate hearing, major PBMs stated they would welcome lower list prices for GLP-1 drugs, and a list price cut wouldn’t harm formulary placement so long as the net cost for their insurance clients remains unchanged 10.

In reality, PBMs wield enormous pricing power over GLP-1 drugs by controlling access and playing manufacturers off one another. While PBMs are motivated to secure the lowest net cost for their clients, the opaque rebate system makes it hard to tell if a truly lowest net cost is achieved and allows PBMs to take a fat cut along the way.

As long as PBM revenue comes from a slice of the drug price, their actions will tend to favor higher prices.

Third-Party Administrators (TPAs): Hidden Costs in Plan Administration

When an employer self-funds its health benefits – paying claims with its own dollars rather than buying insurance – it typically hires a third-party administrator (TPA) to run the health plan. TPAs handle claims processing, provider networks, utilization management, and often the pharmacy benefit – either directly or via a PBM partner.

The expectation is that a TPA will act in the employer’s and members’ best interest to manage costs. However, many TPAs are actually divisions of major insurance companies (surprise!). For example, Anthem’s affiliate administers many employer plans, even if the plan is self-funded 11.

TPAs therefore have their own insurance-aligned incentives and conflicts of interest that can drive up spending, unbeknownst to employers.

Influence on Coverage and Utilization

TPAs help employers design their benefit plans – including whether or not to cover certain medications like weight-loss drugs, and under what conditions. Their advice might be colored by cost considerations (GLP-1 coverage can significantly increase claims cost) but also by competitive pressures (employers want to attract talent with good benefits).

TPAs might impose prior authorization or clinical criteria to control utilization. Importantly, if a TPA is aligned with a PBM, it may follow the PBM’s formulary and coverage rules, which, as discussed, might favor certain high-cost drugs. For instance, if a compounded semaglutide was available and cheaper, a TPA might still exclude it as “not FDA-approved” (and indeed many did, even before FDA’s crackdown, albeit for liability concerns).

Opaque Fees and Secret Overpayments

A less visible issue is how some TPAs extract value through the pricing of claims and services. Because TPAs directly negotiate with providers and PBMs with limited oversight from employers, they might have opportunities to financially benefit from this information asymmetry.

For example, there have been cases where an insurer acting as a TPA negotiated discounts with hospitals or pharmacies but did not fully pass those savings to the employer’s plan. In one lawsuit, a union health fund accused Anthem (now Elevance Health) of unlawfully applying only part of a hospital discount and retaining the difference, effectively overcharging the self-funded plan 12.

Such hidden overpayments can go undetected when TPAs refuse to share detailed claims data. Historically, “gag clauses” in contracts prevented employers from seeing price details. Congress banned these gag clauses in 2021, but compliance remains spotty 13.

The Georgetown University Health Policy Institute has noted multiple court cases in recent years that uncovered questionable TPA conduct, such as hiding data or failing to act in the plan’s interest 14. These practices contribute to excessive health care spending for employers: if a TPA can get away with a slightly higher payment here or there, the employer may never know – but everyone’s premiums and costs inch upward.

TPAs might not grab headlines like PBMs do, but they play a significant role in plan costs. Their influence is more about how costs are managed or hidden rather than drug pricing per se. When it comes to expensive drugs like GLP-1s, there’s even more room for middlemen like TPAs to inflate fees and increase their take – at our collective expense.

Insurance Brokers and Consultants: Incentivizing High-Cost Plans

Employers sponsoring health insurance, whether fully-insured or self-funded, often rely on benefits brokers or consultants to advise them. These brokers help design benefit packages and recommend insurers or administrators. They are supposed to find the best value for the employer and employees.

However, the traditional compensation structure for brokers can pose a serious conflict of interest: most brokers are paid commissions and bonuses by the health insurance industry (surprise!). As a result, brokers may have a financial incentive to favor plans that are more lucrative for them – which predictably correlates more expensive plans that increase overall insurance coverage costs.

How Brokers Get Paid

Typically, when an employer buys a health insurance policy (for smaller companies) or contracts for services (for larger plans), the broker receives a commission from the insurer or vendor. This commission is often calculated as a percentage (e.g. 3–6%) of the total premium or contract value 15. The higher the premium or cost, the higher the broker’s commission.

On top of base commissions, insurers and PBMs commonly offer brokers additional incentives: for example, bonuses for bringing in large groups or keeping clients with the same insurer and even lavish perks like paid trips or exclusive events for top-performing brokers.

A 2019 investigative report by ProPublica revealed brokers were being wooed with “six-figure bonuses to swanky island getaways,” a practice critics called a “classic conflict-of-interest” that can put industry profits above clients 16. Until recently, much of this went undisclosed to employers.

Brokers’ built-in biases towards more expensive plans aren’t limited to insurance plans – this bias can extend to pharmacy benefits as well. As ProPublica reported, “each service provider may provide payments to brokers unknown to the employer” 17 – including PBMs paying a fee for every prescription filled or TPAs paying brokers for each employee added to their plan.

Impact on GLP-1 Coverage Decisions

When it comes to high-cost drugs like GLP-1 agonists, brokers influence the overall plan design and the choice of insurer/PBM. If an employer is debating whether to cover weight-loss medications, a broker’s guidance matters.

Ideally, the broker would present the cost impact and pros/cons objectively. But if, say, the broker’s compensation from the health plan will increase as claims (and premiums) increase, the broker might be less motivated to help the employer contain those costs.

However, brokers know that an unhappy workforce or an uncompetitive benefits package could cost them the client. GLP-1 drugs give brokers a chance to kill two birds with one stone.

Brokers might actually encourage adding a popular benefit like coverage for Wegovy for obesity because it makes the overall plan more attractive. And if the employer’s costs – and thus the broker’s commission – just so happen to increase as a consequence? All the merrier.

Changes and Transparency

Recognizing these conflicts, policymakers have taken steps to shine a light on broker compensation. A new federal law (enacted as part of the Consolidated Appropriations Act, 2021) now requires brokers and consultants to disclose to employers any direct or indirect compensation they receive from insurance carriers, PBMs, or other vendors 18.

Still, the legacy of the commission system means many brokers are essentially encouraged to keep healthcare spending and premiums high. Brokers are not necessarily behind the sky-high price of GLP-1 drugs. But they are unlikely to strongly advocate for aggressive cost-reducing measures if such efforts reduce their own earnings.

The Economics Behind Inflated Prices

Stepping back, we see two major patterns that explain why the U.S. struggles with high drug prices versus other industrialized nations:

Many healthcare intermediaries are compensated in ways that scale with the price of the product or service.

Many healthcare intermediaries are either directly controlled or financially incentivized by healthcare insurance companies.

This latter observation is really worth unpacking. Not only are these healthcare middlemen heavily consolidated within their service area (for instance, the three biggest PBMs control nearly 80% of the market 19), but these middlemen are also vertically integrated with insurers and pharmacies – resulting in healthcare oligopolies.

To demonstrate the immense power that vertical integration affords, let’s study the world’s second largest healthcare company, CVS Health:

CVS Health owns CVS Caremark (a PBM), CVS Pharmacy (retail and specialty pharmacies), Aetna (a health insurer), Wellpartner (a TPA for 340B services) 20, and Oak Street Health (a Medicare-focused primary care provider)

CVS Caremark steers prescriptions directly into its own CVS Pharmacy networks, effectively sidelining independent pharmacies and other competitors.

CVS Caremark can mandate or incentivize Aetna’s vast insurance customer base to use CVS Pharmacies, limiting competition and allowing them to keep profits in-house.

CVS Health has been accused of forcing 340B entities to use its TPA Wellpartner, “effectively forcing covered entities to either forgo substantial savings from the 340B program… or forgo utilization of another TPA that might offer better pricing, quality, or service.” 21

CVS-owned Oak Street Health has been accused of providing health insurance brokers illegal kickbacks in exchange for steering Medicare Advantage enrollees towards Oak Street 22.

This interconnected ecosystem – insurers, PBMs, pharmacies, TPAs, and brokers – creates a powerful cycle of cost inflation, limiting true market competition and keeping American drug prices significantly higher compared to those in other industrialized nations.

Therefore, the nation’s GLP-1 affordability crisis is as much about perversely incentivized middlemen as it is about any one pharmaceutical manufacturer. Unless or until lawmakers, employers, and other stakeholders demand deeper transparency and realignment of incentives, these new weight-loss and diabetes treatments will remain out of reach for too many Americans.

It’s easy to see why each middleman behaves as it does – everyone is just following the money. But after mapping out the pipeline, from manufacturer to insurer to PBM to TPA to broker, it’s painfully clear that the voices that matter the most – those of patients and plan sponsors – aren’t getting much say in how that money flows.

Perhaps the real question, then, is how much longer can this elaborate chain of insurance-controlled profiteers hold out against an increasingly desperate public that is losing GLP-1 coverage and on the financial brink?

Insights from food & health industry leaders at the MISTA Healthy Nutrition Symposium

The GLP-1 Disruption Through the Eyes of Experts

The food industry is facing an unprecedented challenge: a new class of drugs is dramatically changing how people eat. GLP-1 agonist medications – like Ozempic, Wegovy, and Mounjaro – have emerged as powerful appetite suppressants by mimicking a gut hormone that regulates hunger. Originally developed to treat diabetes, they are now reshaping what consumers buy, how they snack, and how companies innovate.

It’s one thing for a new diet craze to ask consumers to choose differently; it’s another for a prescription drug to make them feel differently. As appetite literally shuts down and satiety spikes, major food and beverage categories feel the impact.

Analysts warn billions of dollars of consumer spending are up for grabs. KPMG projects consumers may spend $48 billion less on food and drink each year for the next decade due to GLP-1 use 1. Some of the world’s biggest players – Nestlé, Coca-Cola, Danone, Conagra – are already pivoting to meet the GLP-1 moment.

“We don’t want to be the last guy,” admits Conagra Senior VP Bob Nolan.

So how should the food industry respond? To explore this question, I convened a panel of four experts at MISTA’s 2025 Healthy Nutrition Symposium:

Cate Ward (Semper Organics): Scientist, dietitian, and Stanford University researcher whose work intersects nutrition and microbiome science.

Jenny Zegler (Mintel): Director of global food and drink research at Mintel with 17 years covering food and beverage innovation.

Emilie Fromentin (Givaudan): Head of Explore Health, Functional, and Color at Givaudan, a global leader in flavors, ingredients, and nutritional solutions.

Rocio Martin (Danone): Senior Director of Life Science Innovation at Danone, focused on biotics, proteins, and overall health benefits in food.

Our conversation reveals how GLP-1 medications are reshaping consumer behaviors at a biological level – and how food companies can position themselves to not only survive but thrive in this new world.

The Physiological and Behavioral Impact of GLP-1s on Food Consumption

Changing the Fundamentals of Consumption

The physiological punch of GLP-1 agonists is impossible to ignore. By slowing gastric emptying and blunting hunger signals, these drugs lead people to feel full on far less food.

“These medications reduce the craveability of food and increase satiety,” says Cate Ward. “But they also come with side effects like GI symptoms and nausea.”

Data from Mintel underscores how this plays out in daily eating habits. According to Jenny Zegler:

“Smaller portions are the new norm for GLP-1 users. Yet our research finds 51% of U.S. adults on these drugs increased their snacking compared to the previous year, far surpassing the 25% figure for all U.S. adults.”

This contradiction – snacking more, yet eating smaller total quantities – suggests consumers are reorganizing how and when they eat, rather than blindly restricting all food. Danone’s internal data points to another shift:

“GLP-1 users are consuming smaller meals but more frequently, and more healthy snacks – fruits, vegetables, dairy, high-protein, and fiber-rich foods – while decreasing processed items, sweets, and alcohol,” explains Rocio Martin.

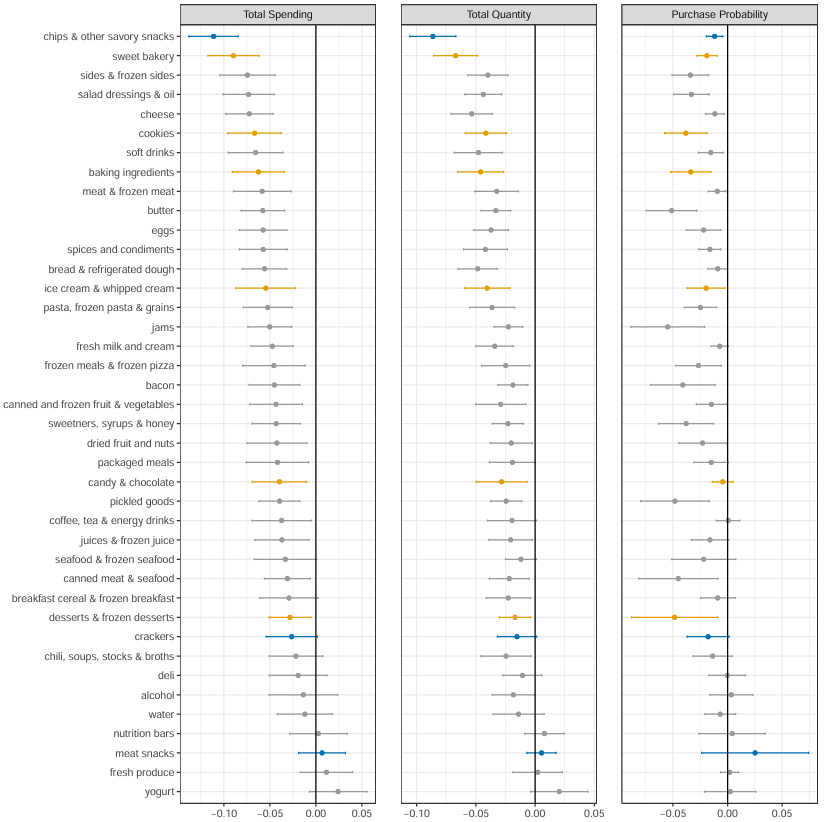

In fact, many GLP-1 households are increasing their spend on yogurt, ready-to-drink protein shakes, and nutrition bars at higher rates than non-users. A recent Cornell study bears this out: in the first six months, savory snack buys dropped 11% and sweet baked goods 9%, while spending on healthy staples climbed 2.

Changes in Grocery Spending Six Months Post GLP-1 Adoption by Category. The No-Hunger Games: How GLP-1 Medication Adoption is Changing Consumer Food Demand

Evolution of Eating Patterns Across the GLP-1 Journey

Food preferences also shift throughout a GLP-1 user’s journey. Early adopters often battle nausea and intense fullness, then pivot to optimizing diet quality once maintenance sets in.

“They start caring about not losing too much muscle and ensuring adequate nutrients in a limited diet,” says Ward, who sees many GLP-1 patients in her private practice. “After stopping the medication, some are determined to keep the weight off by improving diet quality.”

Zegler notes Mintel found that 12%+ of weight-managing adults have previously used GLP-1 drugs, roughly the same share as those currently on them 3. That suggests plenty of former patients need on-going nutritional support.

“There’s a real opening for foods and supplements that replicate that satiety benefit,” Zegler says, “particularly for people no longer on the drug but still keen to manage weight.”

KFF Health Tracking Poll May 2024: The Public’s Use and Views of GLP-1 Drugs

Changes in Taste Perceptions and Food Desires

A less-discussed twist is how these medications may dampen taste perception itself. Emilie Fromentin points to a recent study in Physiology & Behavior showing depressed perception of all five taste qualities – sweet, sour, salty, bitter, savory – among GLP-1 users 4.

“We need more research,” says Fromentin. “But anecdotally, patients report they just don’t crave sweets or certain rich flavors as strongly, which might explain why they gravitate to fresh produce and yogurt.”

Meanwhile, muscle loss remains a key concern. Clinical data shows 15% to 60% of total weight lost on GLP-1 drugs can be lean mass 5 – which has massive potential metabolic downsides.

“Beyond its structural roles, muscle influences glycemic control and metabolism,” says Martin. “Users should focus on high-quality protein intake and resistance training to minimize lean mass loss.”

Some scientists even recommend whey over casein-based proteins, given casein’s clotting effect in the stomach might amplify fullness and reduce intake of crucial nutrients.

Unexpected Changes in Consumer Behavior

Given these complexities, the consumer journey isn’t straightforward. Severe nausea can make patients seek bland, fortified foods on “new dose days,” while intermittent usage patterns mean people may “go on and off” the drug, as Fromentin points out.

“That’s another opportunity: post-treatment solutions. Cost is a big factor, so we expect waves of usage,” she adds. “Food companies should track new drug releases and remain agile.”

Commercial Implications and Market Adaptation

How Early Movers Are Responding

Faced with these seismic shifts, big players are experimenting with different strategies. Danone took the lead in proactively spotlighting existing products suited to GLP-1 users. A dedicated page on its website showcases protein-rich yogurts and shakes.

“Danone NA highlights items that address GLP-1 challenges – muscle preservation, bone density, minimal added sugar,” says Martin. “Coca-Cola touts that two-thirds of its portfolio has low or no calories, Campbell’s pushes nutrient-rich soups, and Nestlé just launched an entire new brand – Vital Pursuits – targeting this demographic.”

Vital Pursuits focuses on portion-controlled frozen meals (250–400 calories) high in protein and fiber. The brand doesn’t mention GLP-1 meds explicitly; it simply bills itself as “High Protein, Portion Aligned, Essential Nutrients.”

On the other end of the spectrum, Conagra is testing an “ON TRACK – GLP-1 Friendly” icon for select Healthy Choice meals, calling out high-protein, high-fiber recipes right on the package. Conagra wants to help GLP-1 users spot these products immediately. It’s a bold approach – more transparent than Nestlé’s stealth branding, but also riskier.

New Foods and Supplements for GLP-1 Users

The lines between food and supplement are blurring. Many GLP-1 users need added nutrients to compensate for lower intake.

“There are parallels between GLP-1 and bariatric surgery patients – both need daily multivitamins,” notes Zegler. “GNC has created dedicated sections for these customers, offering muscle-health, hydration, and energy formulations.”

Danone, for its part, is betting on functional dairy, high-protein snacks, and specialized lines to combat muscle loss. Martin believes in packaging these solutions with education:

“Should you create a specific GLP-1 product line or simply adapt existing SKUs? Either way, bridging knowledge gaps – on muscle preservation, GI side effects, or nutrient deficits – is key.”

Meanwhile, Semper Organics (where Ward works) is exploring how mushrooms and fermentation can deliver nutrients in compact volumes. Ward sees consumer interest in functional foods:

“With new dosage levels come intense side effects, and patients crave gentle, tummy-friendly solutions – fortified crackers, ginger-infused soups, or microbe-based snacks to help with GI symptoms.”

Consumer Response to New Products

So far, the data on consumer response is limited but telling. Some early adopters want explicit labeling (“GLP-1 Friendly!”), but others prefer stealth.

“80% of GLP-1 users are looking for products marketed for their needs, but only 21% want it outright stated on the label,” Martin says, citing a recent Danone-commissioned survey. “It’s a delicate balance: you have to guide them without making them self-conscious.”

Ward sees a clear split: “Some patients want super-clean, less-processed food; others still need convenience. They just want better macros, vitamins, and easy digestion.”

Product Development & Innovation Strategies

Addressing GLP-1 Users Without Alienating Others

Food giants are currently facing a major marketing question: How to reach GLP-1 consumers while ensuring their products also remain appealing for general consumers?

“Using calls like ‘portion aligned’ or ‘excellent source of protein’ resonates with GLP-1 users without explicitly calling them out,” explains Martin. “Retailers can also create store/website sections to cluster these products – think of Walmart’s online gating strategy. But direct labeling can backfire.”

Nestlé tries a middle path with Vital Pursuits, including a QR code that leads curious consumers to a page explaining how the meals are ideal for smaller appetites. By contrast, Conagra’s ON TRACK logo is an experiment in radical transparency.

Specific Product Opportunities for GLP-1 Patients

The panelists agree that muscle preservation is top priority. That means high-quality proteins, plus fiber and probiotics for GI health. Smaller portion sizes are also a must.

“We need to pack nutrients in every bite – whether it’s a compact meal, or a snack that’s bland enough to help with nausea but still delivers protein,” says Ward.

Healthy fats, minimal sugar, plus vitamins D, B12, and iron are also on the radar. Fromentin underscores the potential of advanced flavor systems to help ensure GLP-1 patients are receiving adequate nutrition:

“Taste solutions can help keep the eating experience pleasant despite GLP-1 patients’ reduced taste perception. We’re also leveraging technologies that have been historically utilized for specialized medical nutrition – such as compacting nutrients into small volumes.”

These recommendations align with research showing that 56% of GLP-1 users say they’re opting for more nutritious foods over junk food, 66% report cutting back on soft drinks and alcohol, and 38% are increasing their protein drink intake 6.

Lessons From Previous Health Trends

Our experts see parallels with earlier diet booms, but also big differences. Low-carb, low-fat waves primarily hinged on consumer willpower. GLP-1 reconfigures biology itself.

“We might see some reversion to old preferences, like low-fat to lessen nausea and GI distress,” says Ward, “but each patient’s needs differ drastically. One-size-fits-all solutions won’t cut it.”

Zegler emphasizes:

“Consumers – on GLP-1 or not – still have personal preferences about what to add or avoid. High protein, hydration, and fruits and veggies remain universal for weight loss. The difference is, GLP-1 users feel satisfied faster.”

Long-Term Solutions Beyond the GLP-1 Moment

Looking ahead, new classes of weight-loss drugs may address muscle loss or further alter appetite. Fromentin points out that global expansion is inevitable, with cost the biggest barrier abroad:

“Companies should plan for the day these meds become more affordable or covered by insurance in Europe, Latin America, or Asia.”

Ward adds:

“You can’t just design for the GLP-1 moment,” says Ward. “What about transitioning off the meds? Or layering with new treatments that preserve muscle? Or conversely, products to support lifetime users? Products that adapt with the consumer’s journey will have staying power.”

Zegler reminds us:

“GLP-1 is another tool in the weight-management toolbox. With research pointing to many users only using GLP-1s for a short period of time, it’s smartest for companies to build products that fit the foundations of health and wellness – protein, fiber, hydration, and natural ingredients – rather than try to add labels and formulations to align with the latest craze in weight loss.”

Martin echoes this sentiment:

“Don’t limit yourself to ‘for GLP-1 users only.’ Post-treatment might be even more critical, especially if people rebound or look for gentle ways to keep weight off.”

A Call to Action for the Food Industry

Collectively, the panel drives home a stark reality: GLP-1 drugs have handed consumers a powerful tool to control hunger, and now the ball’s in the food industry’s court to meet consumers’ needs for healthier, more nutritious options. The opportunity is huge, but seizing it requires swift and strategic moves:

Embrace Nutrient Density Every product – from snacks to meals – should deliver more protein, fiber, and micronutrients per bite. This benefits GLP-1 and non-GLP-1 customers alike.

Right-Size Portions and Packaging If shoppers only want a few bites, give them portion-aligned formats. Single-serve packaging or 100-calorie packs can prevent waste and encourage mindful eating.

Communicate Benefits, Not Medications Consumers want help finding muscle-supporting, GI-friendly, or portion-aware products, but don’t necessarily want “GLP-1” emblazoned on the label. Emphasize function (high protein, nutrient-dense) rather than referencing the drug.

Invest in R&D and Partnerships Collaborate with nutritionists, ingredient suppliers, and even fitness brands to tackle issues like muscle loss, taste modulation, and side-effect management. Leverage emerging “compacting” technologies from specialized medical nutrition fields.

Anticipate Future Drug Classes Already, combination therapies are in trials, some addressing muscle atrophy or boosting metabolism further. Stay agile, as the “appetite puzzle” could keep evolving.

Above all, the best hedge is to create robust, healthy foods that align with consumers’ broader wellness goals.

Companies that double down on ultra-processed, empty-calorie products and ignore the GLP-1 trend risk slowly declining as consumers reallocate their dollars. In contrast, those who innovate with quality and wellness in mind can capture not only the GLP-1 segment but also the broader shift of consumers who, with or without medications, want to eat more healthfully.

The food industry stands at a crossroads. GLP-1 drugs have handed consumers a powerful tool to control their eating – and they are using it. Rather than lamenting that people are buying fewer snacks or beverages, smart brands see a chance to become partners in consumers’ health journeys. By delivering products that align with new eating habits, companies can maintain relevance and loyalty.

To the food industry professionals, it’s time to meet the moment: adapt boldly, innovate relentlessly, and help shape a healthier, more resilient food culture for all. Your consumers’ appetites may be shrinking, but their expectations are not – and meeting those expectations is the path to thriving in this new world.

The FDA just ended access to cheaper GLP-1 alternatives – why are the brand-name drugs so expensive?

The End of GLP-1 Compounding Loophole

The Food and Drug Administration’s February 2025 declaration that Novo Nordisk’s Ozempic and Wegovy are no longer in shortage 1 has set off alarm bells for millions of Americans who relied on cheaper, compounded versions of these life-changing medications. This announcement – coming on the heels of a similar ruling in January for Eli Lilly’s tirzepatide (Mounjaro/Zepbound) 2 – effectively ends the regulatory leeway that allowed compounding pharmacies to produce lower-cost semaglutide or tirzepatide. Now, patients who had been paying a fraction of the official price must grapple with $1,000+ monthly costs or risk discontinuing therapy altogether.

Given this shock to the system, it’s worth reexamining a few simple and fundamental questions: why are brand-name GLP-1 drugs so expensive? Why are these astronomical prices a uniquely American phenomenon? And how can we break the cycle and ensure afforable, ready access for the patients who most need these medications?

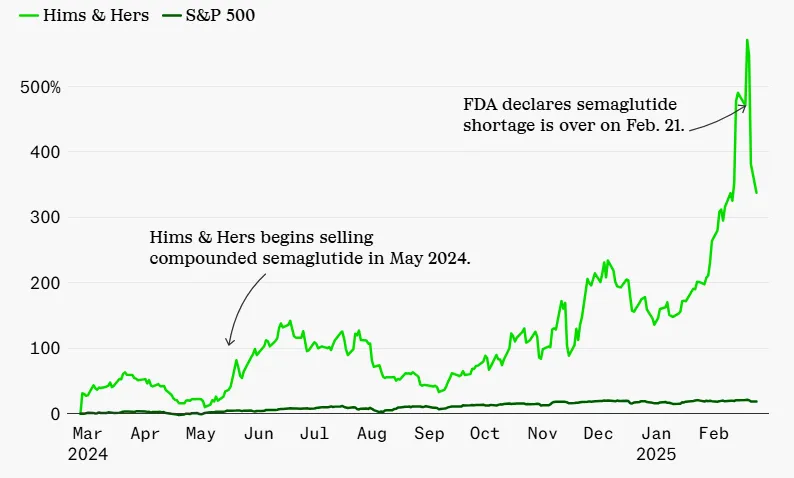

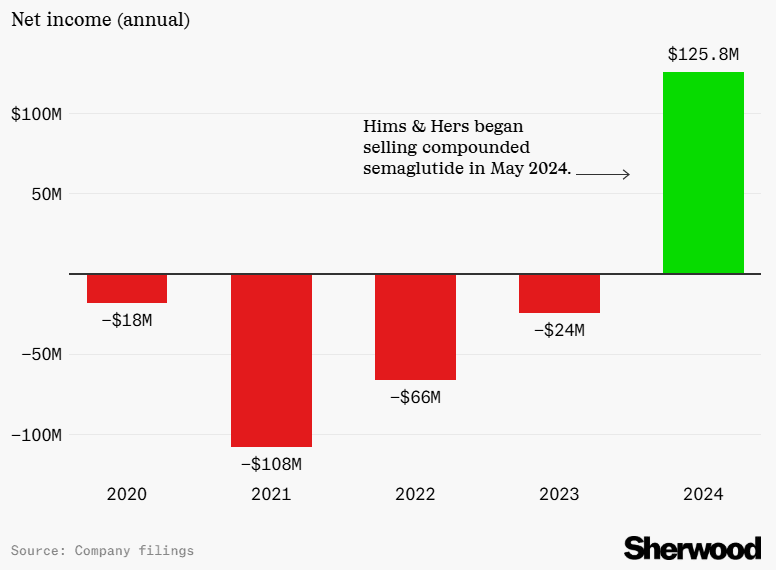

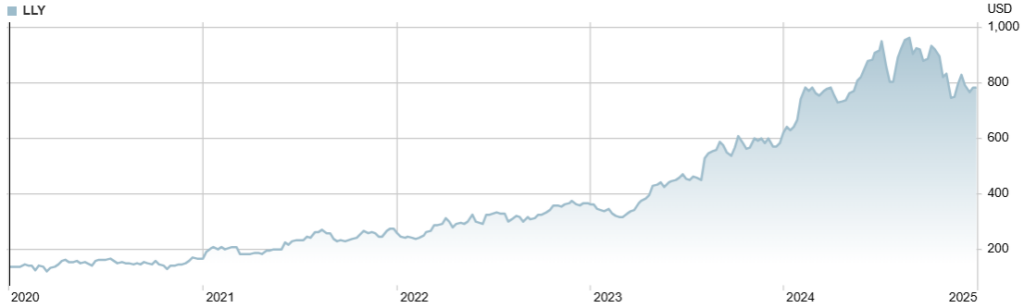

Hims & Hers, a telehealth firm that previously sold compounded semaglutide, saw its stock plummet by 26% following the FDA announcement 3. The company had reported $1.5 billion in annual revenue in 2024 – a 69% increase from the prior year 4 – fueled largely by demand for affordable GLP-1 alternatives. Although Hims & Hers initially pledged to keep offering personalized options, it later confirmed it would discontinue compounded semaglutide by the end of Q1 2025 5.

Hims & Hers five-year net income chart(source: Sherwood).

Alliance for Pharmacy Compounding CEO Scott Brunner worries about the human toll of the ruling. “All we can do now is watch what happens as patients hear the news and try to get a new prescription for the FDA-approved drug.” He notes the “sticker shock” of branded semaglutide puts it out of reach for many patients 6.

Some compounders are challenging the decision in court. The Outsourcing Facilities Association and Texas-based FarmaKeio Superior Custom Compounding filed suit in Fort Worth, alleging that the FDA is “dismissing evidence that the shortage persists” and removing the drugs from its shortage list “without notice-and-comment rulemaking.” 7

Price Shock for Patients

“Today is not a good day for those suffering from chronic disease,” said Noom CEO Geoff Cook, whose digital health company prescribes compounded semaglutide 8. The FDA’s wind-down period allows compounders until April 22 to stop selling copycat versions 9 – giving patients and providers only a brief window to make alternative arrangements. For many, that means confronting the stark reality that the brand-name drugs come with punishing price tags.

While it addresses legitimate safety concerns surrounding unregulated “knockoff” medications, the FDA’s decision exposes deeper flaws in the American healthcare system. It forces a reckoning with short-term economic incentives that render revolutionary treatments inaccessible, even when the long-term medical and financial benefits could be enormous.

Jason Krynicki, Bariatric Insurance Coordinator at Robert Wood Johnson University Hospital and National Board Member of the Obesity Action Coalition, has experienced the economic anxiety of sudden GLP-1 price increases first-hand: “I lost my personal coverage in February 2023 at RWJ – they’re no longer covering obesity medications. I had to tap into my own savings to cover my GLP-1 drugs, which has put me in a really tough spot,” he explains.

Now, with cheaper compounding options phased out, millions of patients who have been taking compounded GLP-1s in the US are about to experience the same price shock. These patients must either pay significantly higher prices for brand-name products, fight for insurance coverage that often doesn’t exist, or give up treatment altogether.

The Price-Value Disconnect: Why GLP-1 Drugs Cost So Much

Manufacturer Margins: A Legal Monopoly

(Source: JAMA Netw Open. 2024;7(3):e243474).

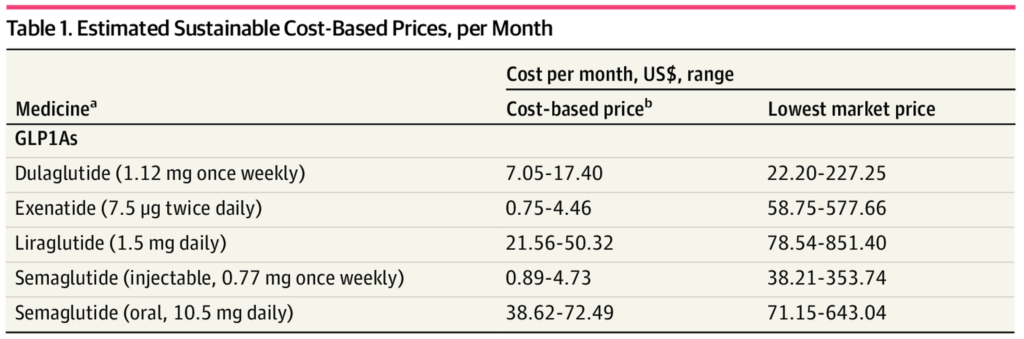

Scrapping cheaper compounded versions shines a harsh spotlight on the massive disconnect between production costs and retail prices for GLP-1 medications. In 2023, a Yale study revealed that a monthly supply of semaglutide can be manufactured for as little as $0.89 to $4.73, yet the list price in the U.S. can exceed $1,000 10. This 21,000% markup is often justified by pharmaceutical firms as necessary to cover R&D costs, clinical trials, and the “innovation premium” that patents provide until the early 2030s.

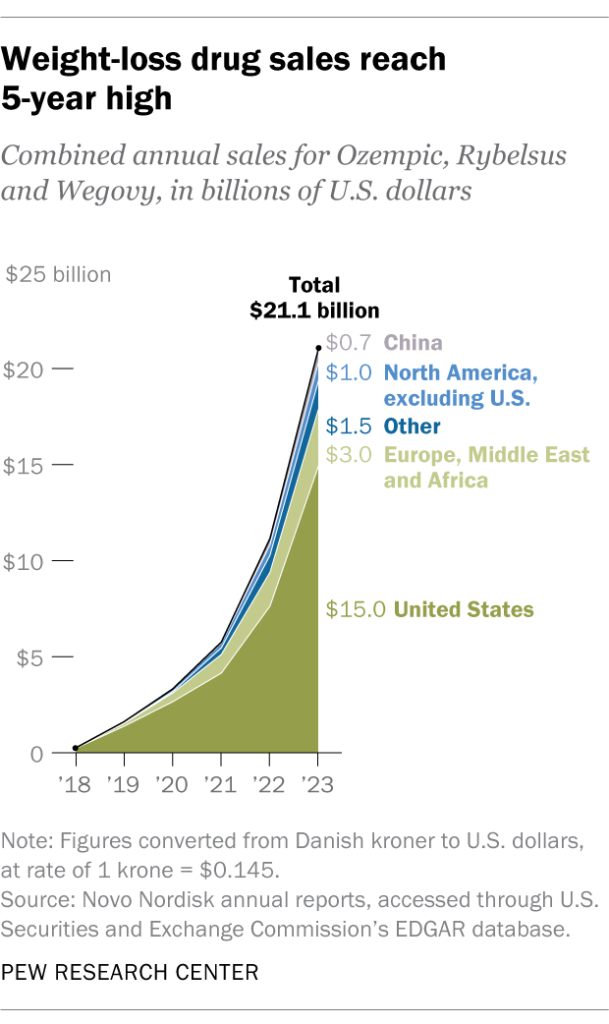

Novo Nordisk and Eli Lilly have capitalized on this exclusivity to maintain premium pricing and post record profits. Novo reported more than $21 billion in combined 2023 revenue for semaglutide (Ozempic, Rybelsus, and Wegovy) alone 11. “Manufacturers are responsible for the ultra-high prices,” argues Krynicki. “They can afford to lower them. The drugs need to be more affordable for people who need obesity care, not just celebrities.”

In a 2024 hearing, Senator Bernie Sanders challenged Novo Nordisk’s CEO on why the same medication costs $969 in the United States but only $59 in Germany – an over 16-fold difference 12. The manufacturer pointed to “significant safety risks” with copycat drugs, praised the FDA for “protecting patients,” and insisted that its $6.5 billion investment this year to expand U.S. production underscores its commitment.

Yet critics remain skeptical that higher supply alone will tame prices, given manufacturers’ inherent profit-seeking incentives. Critics fear manufacturers like Novo Nordisk and Eli Lilly will exploit their temporary monopoly to milk the the GLP-1 cash cow as hard as they can – perpetuating the affordability crisis for patients.

Insurer Incentives: Short-Term Savings

For health insurers, GLP-1 medications pose a thorny financial puzzle. A single patient’s therapy can cost $11,000 or more per year 13 – potentially blowing up budgets if even a modest fraction of eligible members adopt GLP-1 drugs. Now, with the Trump administration reevaluating the Biden administrations decision to require Medicare and Medicaid to cover anti-obesity drugs 14, the stakes could soon escalate.

Insurers are fighting hard against GLP-1 medication coverage for obesity care. AHIP, the largest U.S. health insurer trade group, warns that blanket coverage of weight-loss drugs could “subvert congressional intent” and “bust budgets” if the treatments prove extremely popular 15. Others, like Ceci Connolly of the Alliance of Community Health Plans, argue that “spending big, big bucks on something that still has so many unknowns really jeopardizes the limited dollars and resources that a plan has.” 16

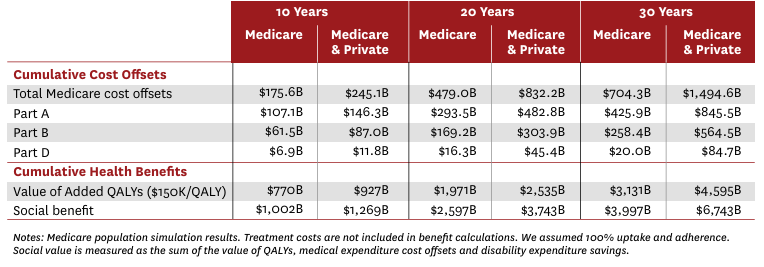

Value to Medicare from Covering and Treating Obesity (Difference from Status Quo)

Yet a 2023 paper from the University of Southern California found that covering weight-loss drugs could save Medicare more than $175 billion to $245 billion over a decade by preventing obesity-related illnesses 17. Dr. Holly Lofton, Director of the Medical Weight Management Program at NYU Langone, emphasizes, “The medications are effective if you can get them – it’s frustrating if you can’t. Insurance access to these meds is the #1 issue in obesity care.”

Part of the problem is what economists call the “turnover problem.” 18 An insurer paying $11,000 for a member’s weight loss this year may never see the payoff if that member switches plans later – a very common occurrence in a society where health insurance is tied to employment and job changes are frequent. This dynamic explains why coverage remains erratic, with companies reluctant to absorb major upfront costs without a guaranteed long-term return.

One former high-ranking insurance executive blames high prices on the underlying profit motive: “insurance companies don’t have a desire for people to be healthier – they make money off people being sick. Doctors fight insurance companies because they actually want people to be well.”

With compounding alternatives disappearing, doctors face a new level of frustration. “Many know how effective GLP-1s can be,” says Dr. Michael Weintraub of NYU Langone’s Endocrinology Department. “But the insurance company is the real gatekeeper. Patients get angry at physicians when they’re denied a known effective tool, and that puts us in a difficult spot.”

Dr. Weintraub’s practice always checks a patient’s insurance beforehand to see if coverage is offered. “More than half of insurers in our area exclude GLP-1 drugs completely,” he notes. Patients shut out of coverage often try suboptimal or risky alternatives, from dubious supplements to black-market medications.

The underlying physiology of obesity also complicates matters. Obesity is a chronic, relapsing condition requiring long-term management. Stopping medication frequently leads to rapid weight regain 19. “Obesity is a chronic condition, and its progressive nature necessitates chronic long-term treatment. If you cease intervention, then the body’s compensatory mechanisms lead to weight regain,” Weintraub explains.

Dr. Marsha Novick, a family physician practicing obesity medicine for 20 years, underscores that “lifestyle changes alone are often not enough for patients with severe obesity. GLP-1s are part of a toolbox that includes meal replacements and even bariatric surgery. Now that they’re more expensive, many patients lose that critical option.”

U.S. Pricing vs. International Models: A Stark Contrast

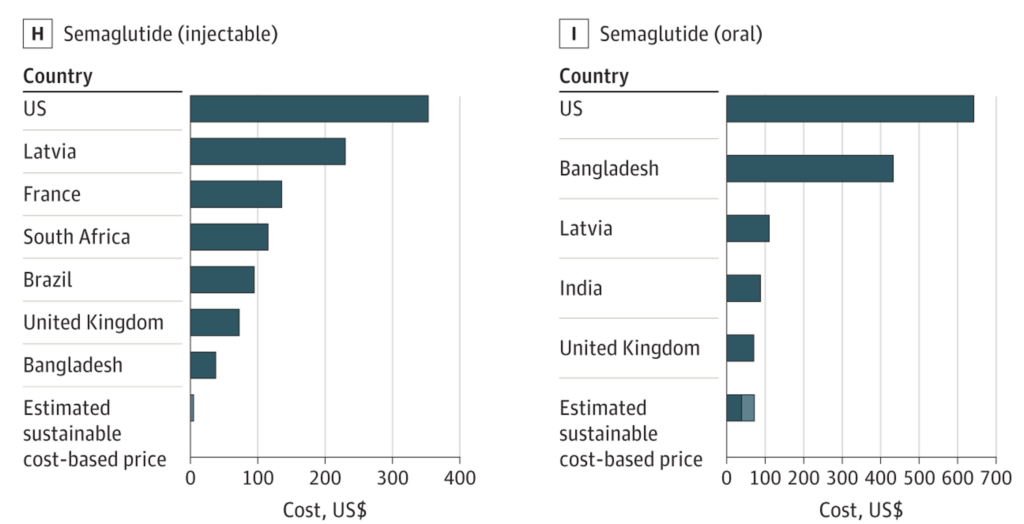

The FDA ruling also spotlights the vast difference between U.S. and foreign GLP-1 prices. In the U.K., Wegovy (semaglutide 2.4mg) has a list price around $160–$220 per pack, while private pharmacies charge $190–$250 monthly 20 – still far cheaper than the American $1,000-per-month price tag. Countries like France, Australia, and Japan report similarly lower costs. A Yale study found some of the lowest market prices worldwide in places such as China, France, the Philippines, and South Africa 21. Unsurprisingly, the U.S. tops the list of highest GLP-1 prices.

(Source: JAMA Netw Open. 2024;7(3):e243474).

Experts attribute America’s outlier GLP-1 prices to:

Lack of Government Negotiation and Price Controls – Most other wealthy nations have centralized negotiating bodies, forcing manufacturers to accept lower rates or face being excluded from coverage. With rate exceptions, the U.S. government doesn’t negotiate drug prices.

Market Size and Ability to Pay – The U.S. is a high-income market accustomed to elevated drug costs. Companies view American patients as profitable enough to bear steep prices.

Regulatory and Patent Landscape – Other countries may get generic or biosimilar competition earlier, whereas the U.S. remains under patent lock until the early 2030s.

Senator Sanders has lambasted manufacturers for “ripping off Americans with high drug prices,” 22 pointing out that Novo Nordisk reportedly derives 72% of its global GLP-1 revenue from the United States alone 23. Novo Nordisk’s revenue concentration is a staggering imbalance and evidence that Americans are effectively subsidizing global R&D costs by paying inflated prices.

The Economics of GLP-1 Medications: A Fundamental Analysis

The abrupt end to compounded alternatives highlights classic economic principles that shape GLP-1 drug pricing in America:

Monopoly Pricing Under Patent Protection

Patents confer a legal monopoly for 20 years (plus extensions). Without competition, manufacturers can charge far above marginal production cost. Semaglutide, for instance, costs under $5 to produce but sells for $1,000-per-month due to Novo Nordisk’s exclusive commercial rights 24.

Inelastic Demand and Value-Based Pricing

Effective obesity treatments are scarce, making demand relatively inelastic – patients and providers are willing to pay high prices when no close substitutes exist. Companies thus set prices based on the perceived value of weight loss and its health benefits, rather than production costs.

Information Asymmetry and Principal-Agent Problems

Patients often lack full knowledge or direct purchasing power, while physicians, insurers, and pharmaceutical companies each have different incentives. This mismatch leads to inefficiencies in how these drugs are prescribed and reimbursed.

The Third-Party Payer Problem

Instead of direct consumer-vendor transactions, insurance plans decide coverage. With each insurer negotiating separately, pharmaceutical firms face less unified resistance to high prices. Patients, for their part, rarely see the full price – until coverage is denied.

International Price Discrimination

Profit-maximizing firms charge each market according to willingness to pay. Because the U.S. tolerates higher prices, manufacturers capture large profit margins here while accepting lower margins abroad.

Short-Term vs. Long-Term Incentives

Insurers are incentivized to maximize immediate profits rather than investing in longer-term outcomes – they might not reap the benefits if a patient changes plans years later. This undercuts coverage for preventive treatments like GLP-1s, despite potential future savings.

Taken together, these factors create a market failure where monopoly power and fragmented insurance lead to high prices and restricted access – even though society might benefit substantially from widespread, sustainable adoption of these drugs. Ending the compounding workaround removes a modest but meaningful counterweight to the monopoly dynamic, further exacerbating the need for direct policy intervention.

Policy Solutions for a Post-Compounding Era

With the loss of compounded options, policymakers, insurers, and drugmakers face renewed pressure to improve access to GLP-1 medications. Several strategies have increased in urgency:

1. Government Price Negotiation

New provisions from the Inflation Reduction Act give Medicare limited authority to negotiate prices on certain high-cost drugs 25. Over time, GLP-1s could be added to the negotiation list once they meet the statutory requirements. If Medicare – the largest single payer – achieves lower rates, commercial insurers might follow suit or be forced to keep up.

Some officials in the Trump administration have signaled interest in allowing or requiring Medicare and Medicaid to cover anti-obesity drugs 26. If approved, it could create a powerful impetus for price concessions. However, insurers caution that covering such treatments broadly could trigger large immediate expenditures, even if it saves money downstream 27.

2. Insurance Coverage Mandates

The Treat and Reduce Obesity Act (TROA) in Congress aims to let Medicare Part D plans cover weight-loss drugs 28 – a key step toward treating obesity like other chronic diseases. Federal Employee Health Benefits plans have already moved to require coverage of obesity meds, setting a precedent. Mandating coverage in commercial markets, too, could spread costs across the entire pool and make therapy more affordable.

3. Patent and Market Exclusivity Reforms

Reforming patent “evergreening” or expediting biosimilar approvals could bring GLP-1 competition sooner, driving down costs. Evergreening extends monopoly protections through minor tweaks, while “patent thickets” delay generic entry even after core patents expire.

Policy fixes – limiting frivolous patent extensions or fast-tracking biosimilars – face legal and political hurdles but could shorten exclusivity and slash prices 29. Critics note many top-selling drugs remain under overlapping patents far beyond their original terms. Whether these reforms strike the right balance between encouraging innovation and preventing monopolistic abuse remains a key question.

4. March-In Rights

In the most extreme case, march-in rights, authorized under the Bayh-Dole Act, could be used. March-in rights allow the government to license a patent to another manufacturer in extraordinary cases – for instance, if the original patent holder fails to make the invention available on reasonable terms 30. Though rarely used, some advocates argue it could be invoked for GLP-1 drugs if sky-high prices effectively block patient access. Drugmakers counter that such a step would undermine the incentive structure for innovation and likely invite legal battles 31.

5. Alternative Funding and Pricing Models

Outcomes-based contracts – paying only if the drug achieves health improvements – could encourage coverage by reducing the perceived risk 32. States have tested “Netflix” subscription models for hepatitis C treatments, paying a flat rate for unlimited patient access 33. A variant of that approach could theoretically apply to GLP-1s, smoothing out the high per-patient costs.

One intriguing idea is a tiered treatment approach: fully cover expensive GLP-1 therapy for, say, a six-to-twelve-month period to achieve major weight loss, then transition to a cheaper maintenance protocol. This two-phase model addresses insurer anxiety about indefinite high costs while still giving patients a viable path.

A Watershed Moment for Healthcare Access

By declaring that semaglutide and tirzepatide are officially off the shortage list, the FDA has inadvertently exposed the underlying fault lines in American healthcare. Patients who relied on affordable compounded GLP-1s must now confront the branded drug’s steep price tags or risk abandoning a therapy proven to curb obesity and related illnesses.

“GLP-1s work, but the access to care needs to be there,” says Jason Krynicki, summarizing the crux of the crisis. Dr. Holly Lofton echoes this sentiment: “These drugs create hope that weight loss is possible – not as a fad diet, but with better results than old interventions. It’s frustrating that cost so often stands in the way.”

Ultimately, true reform requires more than just improved supply. It demands policy changes – whether through government price negotiation, expanded insurance coverage, or patent reforms – that align the long-term economic gains of preventing chronic disease with the short-term realities of medical decision-making and reimbursement.

As obesity continues to rise, GLP-1 medications represent both a remarkable scientific success and a sobering market failure. The end of compounded alternatives should galvanize stakeholders – from Congress to pharma CEOs – to devise strategies ensuring that life-changing therapies do not remain out of reach for the patients who need them most. Until then, the nation’s GLP-1 affordability crisis remains unresolved, underscoring the urgent need to reconcile innovation with equitable access in American healthcare.

Our Sickcare System May Be Luring GLP-1 Patients into a Health Trap

This is the third of our three-part series on The Ozempic Era. This series explores how the Food Industrial Complex engineered an addiction crisis, how Ozempic emerged as its apparent antidote, and why millions of desperate patients betting their health on GLP-1 drugs may be making a deal with the devil.

The true cost of anti-obesity medications extends far beyond their hefty price tag. Up to one-third of patients’ weight loss comes from lean muscle tissue rather than fat 1, severely impairing their metabolic “furnace.” When treatment ends – whether from patient fatigue, insurance denial, or unmanageable costs – the body is thrown off balance. Patients experience a perfect storm of metabolic maladaptation:

Junk food cravings return with a vengeance,

Diminished muscle mass means a lower resting metabolic rate and reduced calorie burning potential, and

Weight rebounds as their bodies, unable to cope with the sudden excess of junk calories, store this energy as fat.

The toll is brutal: this cycle often leaves patients not only heavier than before but metabolically and psychologically damaged.

Their bodies, having lost critical muscle mass and gained proportionally more fat, are even less equipped to maintain a healthy weight.

Their confidence in medical interventions is shattered.

Their financial resources are depleted.

And perhaps most cruelly, their brief taste of freedom from food addiction makes their return to old patterns all the more painful.

Why are the alluring promises of miracle weight loss drugs failing to manifest for so many patients?

The Terms of the Deal

The Seductive Promise

For eight years, Rachel had tried everything. After her first pregnancy left her struggling with gestational diabetes and stubborn weight gain, she cycled through all the standard interventions: nutritionists, personal trainers, specialized diets. Nothing seemed to touch her body’s newfound resistance to weight loss. Three different primary care physicians dismissed her postpartum weight gain concerns with bland advice about exercise and portion control.

When her doctor finally suggested GLP-1 medication, Rachel spent two months researching before agreeing to start treatment. “There’s so much stigma around these drugs,” she shared with me. Her hesitation reflected a common tension: the desperate desire for change tempered by fear of both the medication’s physical risks and the social implications of relying on pharmaceutical drugs for weight loss.

Nevertheless, the transformation, when it came, was profound. The “food noise” that had plagued her for years – particularly during stressful business travel – simply vanished. Previously irresistible treats became unpalatable. Her longtime love of wine gave way to a complete disinterest in alcohol. The siren song of modern processed foods suddenly seemed to lose its allure.

Millions Scramble to Sign on the Dotted Line

Rachel isn’t alone. Mass media and social media alike are filled to the brim with tales of GLP-1 medications’ unprecedented results: 15-20% 2,3 total body weight reduction, greater impulse control, and – most remarkable of all – a fundamental reset of patients’ relationship with food. Stories like Rachel’s serve as a siren call for the millions of Americans who have endured decades of failed diets and relentless weight regain. These medications promise to restore something they once thought lost: hope.

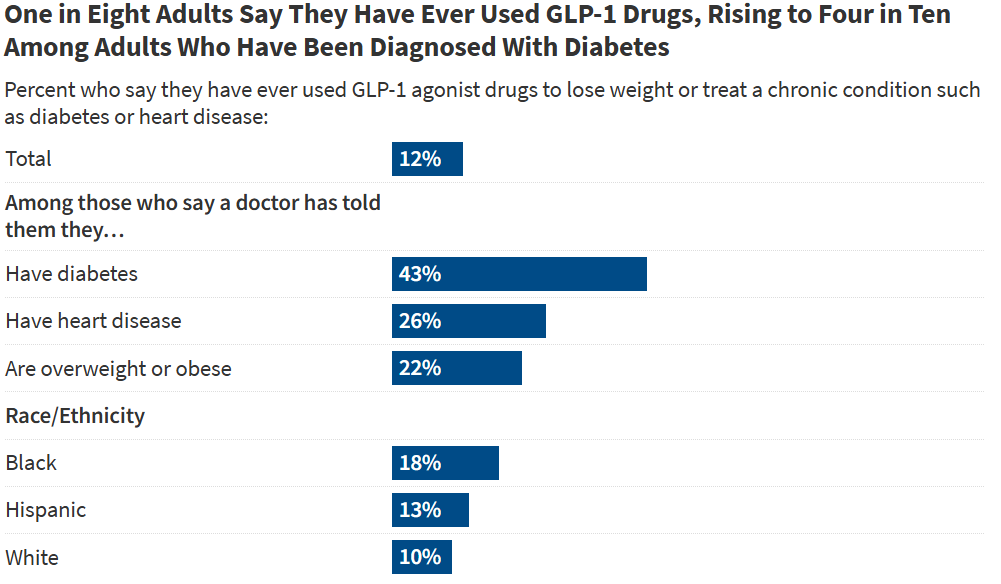

The emergence of compounded anti-obesity medications, available at a fraction of branded drugs’ costs, has further democratized access to effective weight loss treatments. Over one in eight American adults have now tried these medications 4, an unprecedented adoption rate that speaks to both their effectiveness and the desperation of a population where nearly 75% struggle with excess weight 5.

But beneath the alluring promise of rapid weight loss lies a more complicated reality. As the first wave of patients progresses through treatment, concerning patterns have emerged – patterns that suggest these miracle drugs may extract a steeper price than anyone initially realized.

Read the Fine Print

Most patients view GLP-1 medications as a silver bullet for obesity – just pull the trigger to reclaim your body. And why wouldn’t they hold this belief when they are constantly bombarded with articles 6, advertisements 7, and testimonials 8 touting Ozempic and similar drugs as miracle cures?

Yet the pharmaceutical industry’s position, while quietly stated, is clear: these medications are designed for chronic disease management, not short-term intervention. Just as a diabetic patient requires ongoing insulin treatment, manufacturers maintain that sustained weight management requires continuous GLP-1 treatment 9.

This reality conflicts sharply with both patient expectations and physician hopes. While on the medications, patients experience unprecedented control over their eating habits. This dramatic shift can create an illusion of permanent change, masking the critical need for fundamental lifestyle modifications. Many physicians, observing this positive progress, attempt to wean patients off these medications after reaching their target weights.

But very few patients are prepared for the intensive lifestyle changes needed to maintain their progress once treatment ends. Even patients who understand this need face an unfortunate reality: their treatments are often interrupted before new behaviors can take root.

The result is a system that seems almost intentionally designed for failure: patients begin treatment without understanding the fine print, receive inadequate support during their brief – and expensive – window of opportunity, and very likely face financial or other pressures that force premature discontinuation. This combination of factors transforms what could be an effective strategy for fostering long-term healthy habits into a mere temporary reprieve.

Our Sickcare System Is Failing Patients

The Primary Care Brain Drain

In my recent conversations with physicians, a recurring theme became concerningly evident: physicians are tired. Really really tired.

“Medicine is incredibly stressful – we have the highest suicide rate of any profession,” Dr. Laurie Marbas tells me. After two decades practicing medicine, she’s witnessed the steady erosion of primary care on multiple fronts. Crushing medical school debt drives new doctors toward higher-paying specialties 10, while reduced health insurance reimbursement rates and increased denials put intense financial pressure on patients and physicians alike 11. Doctors often bear the brunt of patient frustrations, increasing burnout risk 12.

Dr. Courtney Younglove, who operates two obesity medicine clinics, describes watching talented colleagues abandon private practice for corporate positions that offer escape from the crushing financial and administrative burden. “Everyone wants out,” she says. The exodus leaves fewer front-line physicians available to manage the growing wave of patients seeking weight loss treatment.

Those who remain face impossible demands:

Profit-driven corporate pressure to see more patients in less time 13 has transformed doctors into “cogs in the wheel,” as one physician bluntly put it to me.

The standard fifteen-minute appointment barely allows time to check vital signs 14, let alone provide the comprehensive lifestyle guidance critical for long-term success on GLP-1s.

Increasingly, health systems plug these gaps with undertrained nurse practitioners who lack the medical expertise to manage complex obesity cases 15.

The Obesity Medicine Training Vacuum

The crisis extends beyond physician availability into the foundations of medical education itself. “I was never taught how to incentivize patients and motivate behavior change. I had to learn that on my own,” Dr. Marbas explains, describing a pervasive gap in obesity medicine training. Medical schools provide virtually no instruction in the complex interplay of nutrition, metabolism, exercise science, and behavioral psychology required for successful long-term weight management 16.

This knowledge gap becomes especially dire when prescribing GLP-1 medications, where the quality of lifestyle support can mean the difference between lasting transformation and devastating relapse. Many physicians lack the expertise to help patients preserve muscle mass during rapid weight loss or navigate the psychological challenges of diet change 17,18. Without this guidance, patients lose their brief window of opportunity for developing sustainable habits before treatment ends.

The problem is systemic: medical education remains focused on treating acute conditions while chronic diseases like obesity require an entirely different skill set 19. As one specialist observed, “We have the best acute care system in the world. If you have an acute medical condition, there’s no better country than America for treatment. We have the most cutting edge medical technology on the planet. But you can’t use an acute care model to treat chronic diseases. Our system is designed for sickcare, not healthcare.”

The Missing Support Infrastructure

Despite billions invested in healthcare technology, the basic infrastructure for successful obesity treatment remains absent: coordinated cross-disciplinary care teams, consistent behavior modification coaching, and proven protocols for managing the critical transition off medication.

The consequences of this infrastructure gap become evident in treatment outcomes. Patient after patient describes receiving their prescription with minimal guidance beyond basic dosing instructions. Critical aspects of treatment – preserving muscle mass, managing side effects, preparing for eventual discontinuation – are left largely unaddressed. The assumption seems to be that the medication alone will somehow solve decades of disordered eating patterns.

And that’s for formal, in-person doctor appointments. Many online compounding GLP-1 sellers merely ask patients to fill out a short intake form in order to receive compounded anti-obesity medications. If patients are lucky, these companies will provide education materials regarding diet change, muscle preservation, and side effects management. But for the vast majority of compounded drug consumers, they are left to fend for themselves – relegated to consultations with Dr. Google or their local weight loss Facebook group.

One may propose that recurring telehealth consultations with medical or nutrition experts are the answer. However, attempts to augment patient care with digital education tools or remote coaching have thus far borne little fruit. “Digital health tools keep getting pitched as the solution,” Dr. Younglove tells me, with an air of mild annoyance. “But they’re just adding complexity without really moving the needle.”

Some weight loss clinics augment their care with lifestyle change coaches. However, many coaches’ strategies rely on the old weight loss playbook of calorie counting and motivation, which runs counter to physicians’ efforts to reframe obesity from an issue of poor willpower to one of biology. The behavioral element of weight loss – understanding trauma, addressing emotional eating, building sustainable habits – often gets lost in the rush to show quick results.

Physicians Are Caught between a Rock and a Hard Place

Healthcare providers face a profound dilemma. They witness the medications’ transformative potential: when patients aren’t constantly battling cravings, when their minds aren’t clouded by intrusive thoughts of food, they finally have the headspace to do the hard work of changing their dietary habits.

However, the protocols physicians know their patients need – comprehensive metabolic monitoring, regular lifestyle counseling, structured transition planning – are often impossible to deliver within the constraints of modern medical practice. Physicians are thus forced to watch as their patients cycle through predictable patterns of initial success followed by devastating relapse.

Some physicians also shared with me in private a growing frustration of the quick-fix mindset held by many GLP-1-seeking patients. Doctors increasingly find themselves cast as gatekeepers to medication rather than partners in health transformation.

As trust erodes between patients and providers, the fundamental doctor-patient relationship suffers. Our sickcare system’s failure to support preventative care or lifestyle change mutates what should be a healing partnership into an adversarial dynamic centered around prescription access.

Uncovering Ozempic’s Physiological Traps

During Treatment: Deteriorating Body Composition

When patients begin GLP-1 treatment, few understand the hidden cost to their body’s fundamental architecture. A substantial portion of patient’s weight loss comes not from fat but from lean body mass 20, which consists of muscles, bones, organs, skin, and other non-fat components.

The loss of muscle mass creates changes in body composition that lead to accelerated biological aging, setting up conditions for a cascade of metabolic complications 21. Studies also show significant reductions in bone mineral density, which is particularly concerning for premenopausal women 22.

“For all weight loss, you’re losing both fat and muscle,” explains S.M., a dietitian who has spent her career working with eating disorders. “But when you regain weight, it comes back primarily as fat unless you’ve maintained adequate protein intake and resistance training throughout treatment.”

This asymmetric pattern of fat + muscle loss followed by fat regain progressively erodes patients’ lean mass. Even if patients successfully achieve their target body weight, they may experience “skinny fat” syndrome – a form of metabolic obesity where their normal weight masks a high body fat percentage and dangerous metabolic dysfunction 23.

The physician oversight gap compounds these challenges. Many prescribers – particularly online providers – provide little information about avoiding muscle loss. Without proper guidance on nutrition and exercise during treatment, patients unknowingly sacrifice the very tissue they need most for health and longevity. More troubling still, this deterioration occurs silently, masked by the euphoria of watching the numbers on the scale decrease.

Post-Treatment: Metabolic Dysfunction